Hey, I'm Danny! If you're new, hit subscribe below to join a community passionate about mastering personal finance. Your support means a lot – thanks for being part of the journey!

"Whenever you want to change your behavior, you can simply ask yourself: How can I make it obvious? How can I make it attractive? How can I make it easy? How can I make it satisfying?"

- James Clear

I just finished reading the book Atomic Habits by James Clear, which just happened to coincide with the writing of my money management via SoFi article. The book aims to offer the reader a simple formula for creating good habits, and breaking bad ones. The main argument being that small incremental changes to the systems that govern our behavior contribute the most to our success in life. In my article “Getting your money right with SoFi” I talked about, before anything else, developing a money move mindset. I consider this the most important step to becoming successful with your money. You can read that article here:

Getting Your Money Right With SoFi

In this article I want to take James Clear’s ideas and use them to go into greater detail of how to shape your behavior towards a money move mindset. We all come from different backgrounds and have unique ways of doing things. Money management isn’t a one size fits all system and what works for me isn’t always going to work for someone else. That being said, my hope is for this article to help you find out what does work for you, and how SoFi can be leveraged to fit your needs.

The Four Stages of a Habit

First let’s look at the four stages of a Habit:

Cue

Craving

Response

Reward

This is essentially the breakdown of how a habit forms. A cue triggers your behavior to begin, craving is the desire to perform that behavior, response is you acting to fill that craving, and then when finished you feel rewarded. Applied to something as simple as making a cup of coffee in the morning, your cue is waking up, your desire or craving for alertness pushes your response to get that fresh brew going, and you’re rewarded with your caffeine fix. Do it enough times and it becomes second nature to you, it’s just what you do every morning.

In order to develop new habits Clear stresses to

Make It Obvious

Make it Attractive

Make it Easy

Make it Satisfying

Let’s say you want to start reading for 10 minutes a day, it’s beneficial to attach that action to a time and place. “I will read 10 minutes a day when I get to my desk in the morning.” In order to keep coming back to it, make it attractive, for example by reading about topics that you enjoy or doing it with something else you already enjoy, like drinking your morning coffee. Make it easy by leaving the book on your desk so it’s waiting for you in the morning, or by using audible to read for you. We naturally gravitate towards what is easiest, and stray away from what’s too difficult. To keep things easy, start with just a page a day and build on that as it becomes routine. Finally, make it satisfying by tracking how much you’ve read and rewarding yourself as you reach milestones. This could be as simple as a checkbox in your calendar signifying each day you read, or getting your favorite food each time you finish a book. Any action that comes with reward is naturally more likely to be repeated.

So that’s how this works or at least how I understood it. Now let’s look at some ways to apply these concepts to managing your money:

Identifying your Money Personality

Being successful with your money isn’t about how smart you are or how much you make, it’s directly correlated with your behavior, and your behavior is formed through a mix of biological, social, and environmental factors. Growing up in extreme poverty may force someone to develop a scarcity mindset, which could lead to either impulsive spending (spend it while you have it) or hoarding every last penny. The key to breaking out of your shaped behavior is by being aware of it in the first place. Without sitting down and analyzing the way you spend, borrow, and invest you’ll never have a clear picture of how to move forward. Clarity is key to financial peace. You may think you know how you act, but never know the full extent of it until it’s on paper (or on screen) in front of you.

Again, I talk about and recommend how to use SoFi to track your money easily here:

Getting Your Money Right With SoFi

Here are some personality traits that could be affecting how you act with your money:

Spender vs. Saver:

As mentioned before, you may be more relaxed while spending your money on yourself or others, or want to save every penny you make.

Risk-Taker vs. Risk-Averse:

Some people are much more willing to take risks with the money they have in hopes for better returns, and some prefer playing it safe.

Impulsive vs. Disciplined:

You may be more inclined to make spontaneous purchases without much thought instead of being deliberate and carefully weighing each purchase.

Materialistic vs. Minimalist:

You may value things of higher quality, or find it necessary to obtain status symbol products compared to someone who prefers to live with less.

Nerd vs Free Spirit:

You may thoroughly enjoy digging into the financial data (like me), or you may cringe at the thought of making a budget.

None of these are inherently bad, they make you you. However, if being too skewed towards one side of these traits is affecting your ability to get your money right then it becomes problematic. The goal is to find balance. Having a saver mentality may work in your favor if you’re trying to save money, but it also may interfere with your ability to experience new things in life. Being too risk-averse may protect you from economic downturns, but it also prevents you from capitalizing on the good years and having your money work for you. Identify your behavior, and work towards a reasonable balance that works for you.

Spender:

If you tend to want to spend your money as soon as you get it or enjoy spending on yourself and others, consider a “pay yourself first” budget. Identify how much you can comfortably save each paycheck, and automatically route that amount each month to your savings account each time you get paid. SoFi makes this incredibly easy with autopilot and vaults.

With your savings contribution being already accounted for with each paycheck, you are able to spend the rest on what you value guilt free while still working towards your financial goals.

If you are unable to save comfortably like this, then it may be time to consider cutting back on things that don’t align with what you value. With your money tracked you’ll be able to identify these areas easier.

Saver:

Live a little. I myself am a saver, I’ve hoarded things my whole life, whether it was candy on Halloween, XP in video games, or money now in adulthood. It’s in my nature to want to hold onto every dollar, but again if not regulated it will lead to missing out on experiences that would have been worth the money spent.

If you are actively investing and have paid off all your debt, allocate some money each month to live a little. I call this a fun fund, you can call it whatever you want.

Impulsive:

If you often make impulsive purchases that you later regret, there are a few things you could practice in addition to a pay yourself first budget. If you’re buying things online, delay your purchases for 24 hours before hitting check out. If you still want the item after 24 hours go ahead and buy it. You just eliminated the impulse out of the equation by doing this. Another thing you could try is transferring money into your savings account with each purchase you avoid. Skipped your morning coffee? Move five dollars into your savings account. It will feel rewarding to progress towards your savings goals even faster than by just what you allocate in your budget.

Disciplined:

When being too disciplined in your spending prevents you from making purchases that would otherwise be beneficial to you, practice making routine purchases.

What works for me is adding a “30 minute improvement” chore to our chore list. Clear calls this “habit stacking” by tying a new habit to something you already habitually do. I basically think about what could be bought that would add value to our life each week, and buy it. This helps reinforce the idea that spending money sometimes isn’t going to kill you.

Risk-Taker:

Taking on risk is the key to building wealth. Taking on too much risk is the key to destroying wealth. If you’re inclined to want to swing for the fences when it comes to investing, limit it to a comfortable percentage of your portfolio.

Your goal is to stay in the game for as long as possible, this is how compounding rewards you the most. Sometimes it's better to do what’s reasonable for you, rather than what’s rational. I’ll give you an example:

The reasonable thing to do when it comes to investing is to automate X amount of dollars each month to an index fund that tracks the S&P 500. Get your 10% annual returns and don’t look at it until you retire.

To me that’s boring, even though I know I most likely won’t outperform the S&P 500, it’s more enjoyable for me to hand pick my own stocks. I keep a 50/50 balance of diversified ETFs and individual stocks.

If one of my individual stocks goes broke I’m not discouraged from continuing to invest because my other responsible positions are unaffected.

Risk-Averse:

Being completely risk-averse prevents you from enjoying the compounding effect that is so important to building wealth.

If your goal is to be able to retire, it’s likely that storing your money away under your mattress isn’t going to cut it.

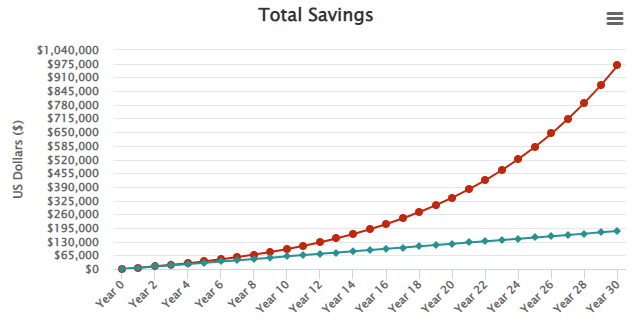

Compare the two charts saving $500 a month with no compounding effect vs the average return of the S&P 500.

Employee sponsored retirement plans are great for this. Out of sight out of mind, and you can’t touch it until you’re of retirement age.

Again the key to building wealth is to stay invested, through the good times and the bad times.

Regardless of your current money traits, here are some things to consider according to James Clear’s four steps to behavior change:

Make it Obvious

The best thing you can do when it comes to mastering your personal finances is to make your finances visible. Make your financial goals visible, write them down and put them on your fridge or your planner, whatever works best for you. Then track your spending and make sure you’re reaching those goals. My recommendation for this is always going to be to use SoFi’s Relay Insights tool.

Make it Attractive

Use visual representations of your finances to help motivate you towards your goals.

SoFi Insights for example will track your loan payoff or savings progress for you. Think about what being financially free would bring you in your life.

Make it Easy

Set up automatic payments and automatic transfers. Use a budgeting application (like SoFi Relay Insights) that will automatically log your transactions and categorize for you, instead of using a spreadsheet. Consolidate your accounts so you have less accounts to pay attention to. Don’t try to do too much at once and remember that small incremental changes to your behavior compound to make a huge impact over time.

Make it Satisfying

Tracking your progress towards financial goals routinely and celebrating when you hit financial milestones, like paying off a credit card or reaching a savings goal, can make things more satisfying.

Self reflection that drives actionable change will help you establish a money move mindset.

"You do not rise to the level of your goals. You fall to the level of your systems." - James Clear, Atomic Habits

That wraps up this week's post. Looking forward to sharing more exciting content with you next week!

Give that like button a tap to help others discover this newsletter if you enjoyed it. If you haven't subscribed yet, hit that button too!